Stamp duty on commercial property must be paid when purchasing a commercial building, a development plot, or a mixed-use property that includes business premises.

However, this tax isn’t just due when the transaction is completed. You will also be liable to pay Stamp Duty on lease premiums, rent, freehold transfers, grants of leases, and any transactions that give you possession or ownership of the property.

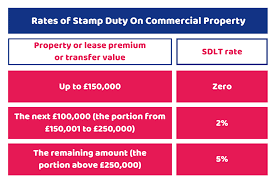

With stamp duty on commercial property rates reaching up to 5%, it can be one of the largest upfront costs for investors and owner-occupiers in the UK commercial property market.

Understanding how stamp duty on commercial property works can save money and prevent unnecessary stress.

Whether you’re buying your first office space or expanding your property portfolio, it’s important to grasp the nuances of this tax.

This guide will simplify the process, breaking it down into easy-to-follow steps while avoiding unnecessary jargon.

Understanding Stamp Duty on Commercial Property

If you’ve ever bought a house, you’re likely familiar with Stamp Duty.

If you’ve ever bought a house, you’re likely familiar with Stamp Duty.

But did you know that Stamp Duty also applies to commercial properties?

For many business owners, navigating the rules surrounding Stamp Duty Land Tax (SDLT) can feel overwhelming.

However, understanding the basic principles and key factors affecting Stamp Duty allows you to make informed decisions and avoid costly surprises.

Stamp Duty Land Tax (SDLT) is a tax that applies when purchasing properties or land exceeding a certain price threshold in England and Northern Ireland.

This tax affects both freehold and leasehold purchases, regardless of whether the property is bought outright or via a mortgage.

SDLT rates vary based on the property type (residential or non-residential), the buyer’s circumstances (e.g., first-time buyers), and any applicable reliefs or exemptions.

Understanding SDLT is essential for accurately calculating the costs of property acquisitions. The tax becomes payable in cases such as buying a freehold or leasehold property, acquiring a property through an ownership scheme, or transferring property in exchange for payment.

However, there are situations where SDLT does not apply. These include:

- Property transfers resulting from divorce.

- No payment is being exchanged for property transfer.

- Inherited properties.

- First-time buyers purchasing properties valued under £300,000.

- Freehold properties purchased for less than £40,000.

- Leases of fewer than seven years where the paid amount is under the SDLT threshold.

Understanding these exemptions can help property buyers make informed financial decisions.

However, when buying a commercial property in the UK, you must pay stamp duty on the property as part of the purchase process.

Savvy investors often look for ways to reduce stamp duty liability or explore exemptions, especially since large sums can significantly impact the overall property cost.

To help you navigate this tax, here are some expert tips on stamp duty on commercial property in the UK.

Tips on Stamp Duty

Commercial property can be a valuable business asset and a smart investment, but it’s important to have the right legal guidance to make sure any property deal you make aligns with both your short-term and long-term goals.

Commercial property can be a valuable business asset and a smart investment, but it’s important to have the right legal guidance to make sure any property deal you make aligns with both your short-term and long-term goals.

With the proper advice and support, you can confidently navigate the process and make the most of your investment.

Since stamp duty on commercial property can vary between regions and may involve complex calculations, it’s important to seek professional advice that’s tailored to your specific circumstances.

By staying informed and exploring available reliefs and strategies, you can minimize your tax liabilities and make your property purchase more cost-effective.

1. Understand the Basics: The basics like the value of the property, the rate, exemptions, and reliefs. Stamp duty on commercial property is typically calculated based on the property’s purchase price.

The rates can vary depending on the value of the property and the region or country where it’s located. It’s important to be aware of any exemptions or reliefs that may apply to your situation.

For example, first-time buyers, small businesses, or charities may qualify for reduced rates or full exemptions. Knowing these basics can help you avoid overpaying and ensure you’re prepared for this cost.

2. Seek Professional Advice: Consulting a tax advisor who specializes in property transactions is a smart move when dealing with stamp duty on commercial property.

They can offer personalized advice based on your specific situation, helping you understand exactly what you owe and whether you qualify for any relief.

Your conveyancer or solicitor can also assist in calculating the tax and ensuring all the paperwork is filed correctly.

3. Explore Potential Reliefs: If you’re a small business owner, you might be eligible for reduced stamp duty on commercial property rates.

In some regions, first-time commercial property buyers may also benefit from lower rates. Non-profit organizations like charities could be exempt from paying Stamp Duty altogether or receive reduced rates.

However, be mindful of any anti-avoidance measures that prevent attempts to artificially reduce Stamp Duty through complex transactions.

4. Consider Timing: Timing can be crucial when purchasing commercial property. If possible, consider scheduling your purchase around the end of the tax year to potentially benefit from certain reliefs or thresholds.

Additionally, keep an eye on property valuations. If the value of the property drops before you complete the purchase, you might end up paying less in stamp duty on commercial property.

5. Explore Alternative Structures: There are other ways to reduce your stamp duty on commercial property liabilities. One option is forming a joint venture with another party, which can potentially reduce individual tax liabilities. Setting up a Special Purpose Vehicle (SPV) to structure the transaction may also help minimize the amount of Stamp Duty owed.

6. Stay Updated: Stamp Duty laws and regulations can change over time, and these changes might impact your transaction.

Staying informed about the latest updates is essential to ensure you don’t miss out on opportunities to minimize your stamp duty on commercial property costs.

How to Calculate Stamp Duty for Commercial Real Estate

Stamp duty on commercial property is a tax imposed on property transactions and can be a major expense when buying commercial real estate.

Stamp duty on commercial property is a tax imposed on property transactions and can be a major expense when buying commercial real estate.

While the basics of how it’s calculated are straightforward, it’s crucial to get professional advice tailored to your specific circumstances.

Here’s a general guide to help you understand the process:

1. Determine the Property Value: The main factor in calculating stamp duty on commercial property is the property’s purchase price or market value.

The higher the value, the more stamp duty you’re likely to pay.

2. Identify the Applicable Stamp Duty Rate: Stamp duty rates vary based on the property’s value and the location (jurisdiction) of the property. As a rule, higher property values come with higher stamp duty rates.

For example, a property worth over a certain threshold may be taxed at a higher percentage than one below it.

3. Calculate the Stamp Duty Amount: Once you know the property value and the stamp duty rate, multiply the two to calculate the total stamp duty on commercial property you’ll owe.

For instance, if your property is valued at £1 million and the stamp duty rate is 5%, you’ll owe £50,000 in stamp duty.

4. Consider Exemptions and Reliefs: Many regions offer exemptions or reliefs that can lower the amount of stamp duty on commercial property you’ll need to pay.

These include:

- First-time buyer relief: For those purchasing commercial property for the first time.

- Small business relief: If you meet certain criteria as a small business, you may qualify for a reduced rate.

- Charity relief: Non-profit organizations often receive exemptions or reduced rates.

- Special property types: Some properties, like industrial or agricultural buildings, may be taxed differently or qualify for special exemptions.

5. Factor in Additional Charges: In some cases, there may be additional fees related to the stamp duty process.

These could vary based on your location or the nature of the transaction.

Example Calculation:

If you’re buying a commercial property valued at £1 million and the stamp duty rate is 5%, your total stamp Duty on Commercial Property would be £50,000.

However, if you qualify for a relief that reduces the taxable value to £800,000, you’d only owe £40,000.

Stamp Duty on Commercial Property laws can be complicated and are often subject to change. To ensure accurate calculations and to check if you qualify for any reliefs or exemptions, it’s highly recommended that you consult a tax professional or conveyancer familiar with the laws in your area.

They can guide you through the process, ensuring you stay compliant and avoid unnecessary costs.

Read Also: Understanding Home Buyers Insurance: 6 Essential Information

Join The Discussion