The Bank of England’s interest rate hike comes at a time when concerns about inflation are growing. This increase has already impacted the mortgage and property markets.

Experts believe that equity withdrawal from the housing stock is one of the reasons consumer spending has remained high, even as the economy slows down.

While housing activity is showing signs of moderation, it would take a more severe downturn to significantly curb house price inflation.

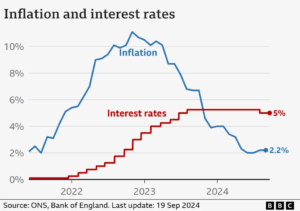

With short-term interest rates now at 5%, there is concern about the impact on two of the Bank of England’s key objectives: controlling inflation and maintaining financial stability.

Although the new Bank of England governor has not yet raised interest rates beyond 5%, he has signaled that further increases may be necessary if inflation risks continue to rise over the next two years.

This situation highlights the delicate balance the Bank must strike between cooling inflation and avoiding disruption in the housing market.

Why the Bank of England Raised the Rate

The Bank of England’s interest rate hike is a direct response to rising inflation, which has been driving up the cost of living for many.

Inflation happens when prices for everyday goods and services increase, eroding the value of money. To tackle this, the Bank raises interest rates to make borrowing more expensive, which in turn helps slow down consumer spending and ease inflation.

In simple terms, an interest rate reflects the cost of borrowing money or the reward for saving it. The Bank of England’s base rate is what it charges lenders when they borrow money.

This base rate directly impacts the interest rates those lenders charge their customers for things like mortgages, as well as the returns they offer on savings accounts.

The Bank adjusts its rates—up or down—to manage UK inflation, which is the rate at which prices rise over time.

When inflation is high, the Bank of England’s interest rate is aimed at bringing it back down to its 2% target by encouraging people to spend less and save more.

Once inflation starts to fall, the Bank may decide to hold rates steady or even lower them, depending on economic conditions.

The Impact of the Bank of England’s Interest Rate Hike on Mortgages

The Bank of England’s 5% interest rate hike is already having a noticeable impact on mortgage rates and housing affordability in the UK.

Here’s how it affects homeowners and potential buyers:

1. Higher Mortgage Rates: When the Bank of England raises its interest rate, commercial banks typically respond by increasing their lending rates, including those for mortgages.

As a result, borrowers will face higher monthly repayments. The degree to which mortgage rates rise depends on competition among banks and their pricing strategies, but it’s generally expected that mortgage rates will climb in line with the Bank of England’s interest rate hike.

2. Reduced Affordability: With higher mortgage rates, monthly payments become more expensive.

2. Reduced Affordability: With higher mortgage rates, monthly payments become more expensive.

Making it harder for both first-time buyers and existing homeowners to manage their loan repayments.

Lenders may also tighten their lending criteria, reducing how much people can borrow.

This could make it more difficult for potential buyers to afford their preferred property.

As affordability decreases, demand for housing may slow down, potentially leading to a dip in house prices and cooling off the property market.

3. Wider Economic Effects: Higher mortgage costs can reduce disposable income, leaving people with less to spend on other goods and services.

This can slow down consumer spending, which in turn could impact industries connected to housing, such as construction, home furnishings, and renovation businesses.

A sluggish housing market can ripple through the broader economy.

While the full effects of the Bank of England’s rate increase may take time to become clear, the immediate outcome is a rise in mortgage rates and reduced affordability for many homebuyers.

As the situation develops, other economic factors could influence the overall impact, but for now, housing costs are on the rise.

The Impact of the Bank of England’s Interest Rate Hike on Property Market

It is important to note that the full impact of the interest rate hike may take some time to materialize, and the situation could evolve as other economic factors come into play.

It is important to note that the full impact of the interest rate hike may take some time to materialize, and the situation could evolve as other economic factors come into play.

However, the immediate effect is likely to be a reduction in demand for property and a potential decline in prices.

The Bank of England’s interest rate hike has several potential impacts on the property market:

1. Reduced Demand: With the Bank of England’s interest rate hike in effect, borrowing money for a mortgage has become more expensive.

This means fewer people can afford to buy homes. Even for those who can afford the initial payments, rising interest rates make the total cost of the mortgage higher over time, making homeownership less accessible for many.

2. Lower Property Prices: As demand decreases, fewer buyers are competing for homes, which can drive property prices down.

Some sellers may resist lowering their asking prices at first, but if their homes sit on the market for too long without selling, they might have to adjust their expectations and reduce prices.

3. Impact on Landlords: Landlords who rely on mortgages to finance their properties are also feeling the pressure of the Bank of England’s rate hike.

Higher mortgage payments reduce their rental income, and with tenants potentially struggling to afford higher rents, landlords may face increased vacancies or lower rental yields.

4. Impact on the Economy: A slowing property market doesn’t just affect homebuyers and landlords it can also hurt the wider economy.

Industries connected to housing, such as construction, home improvement, and furniture, may see a decline in business.

With more of their income going toward housing costs, consumers have less money to spend on other goods and services, which can lead to broader economic challenges.

In summary, the Bank of England’s interest rate hike will have significant effects on the mortgage and property markets.

Homeowners and buyers alike will face higher costs, but by understanding your options and staying informed, you can make the best decisions for your financial future.

Read Also: Can You Get a Mortgage on Benefits? Essential Guide to Options

Join The Discussion